Bitcoin’s derivatives market gave us the best explanation of this week’s macro stress.

Funding rates turned sharply negative, open interest stayed elevated, and then the US jobs report landed. Put together, that showed a market leaning hard into downside hedges just as a real macro catalyst arrived.

That sequence is worth understanding because it explains how macro volatility shows up in crypto.

It usually appears first in perpetual futures, where traders hedge fastest and use the most leverage.

Funding tells you which side is paying to stay in the trade, open interest tells you how much positioning is still in the system, and liquidations tell you when that positioning starts to break.

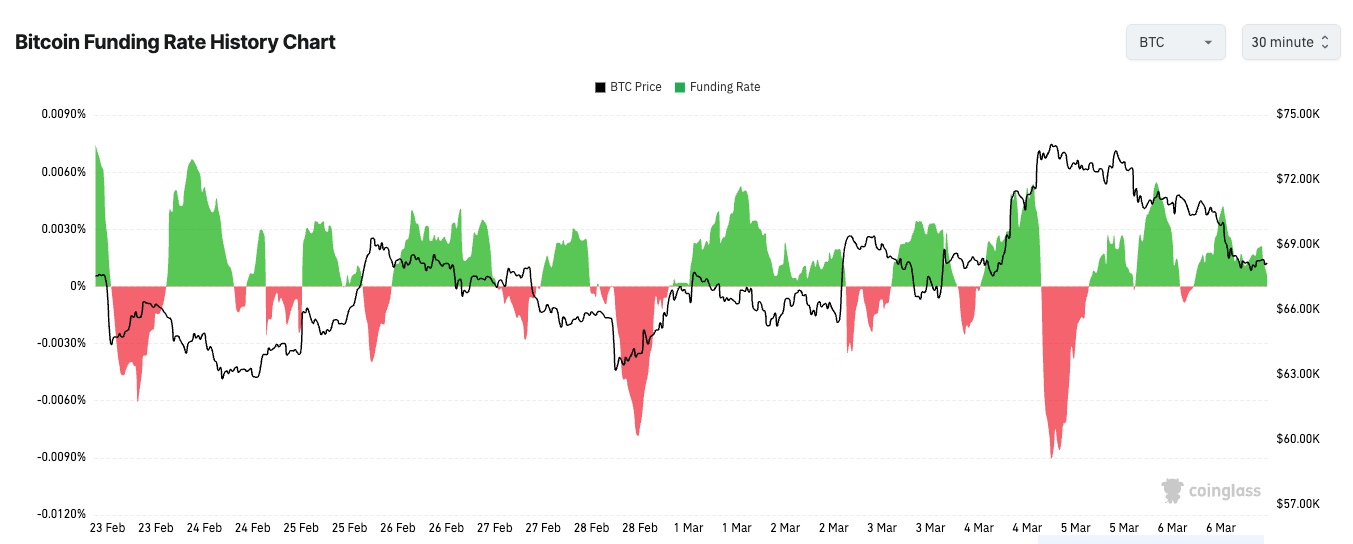

On Feb. 28, perpetual futures funding on Bitcoin fell to around -6%, one of the most negative readings in three months. BTC-denominated open interest rose from about 113,380 BTC to 120,260 BTC since the beginning of the year.

That combination mattered because it pointed to two things at once: traders were leaning heavily into downside bets, and they were doing it with more leverage entering the market. The market was both very nervous and very crowded.

That is the easiest way to understand how macro stress moves into crypto.

It appears in the derivatives book, not as a polished narrative on X or a clean economist note. Traders move there first because perpetual futures are liquid, cheap to use, and always available.

When they get nervous about growth, rates, or a broader risk-off move, they short perps; those contracts slip below spot, and funding turns negative because shorts have to pay longs to keep positions open.

Why negative funding stays negative

But negative funding isn’t a bottom signal in itself; it just tells you where the market is leaning.

This distinction matters because traders like turning every extreme reading into a prediction.

Deeply negative funding can precede a short squeeze, and last week’s setup clearly created that possibility. It can also stay negative for longer than people expect when the hedging demand is real.

Extreme funding spikes and drops reflect one-sided positioning and can persist during strong directional moves.

That persistence usually comes from two places.

Some traders are hedging real spot exposure, which means they aren’t trying to call the exact next move, just trying to protect a portfolio. Others are simple trend-followers willing to pay carry as long as the market keeps moving their way. Both groups can keep funding negative even when the first panic has already passed.

That’s why the real tell is not that the funding is negative. The more interesting setup comes when funding stays meaningfully negative for a while and price stops making new lows. That’s when the pressure starts to build under the surface. Shorts are still paying to stay in position, but the market is no longer rewarding them in the same way. That’s how squeeze conditions form.

The jobs report gave the market a real macro input

The macro catalyst this week came from the US labor market. On March 6, the Bureau of Labor Statistics said nonfarm payrolls fell by 92,000 in February, and the unemployment rate was 4.4%.

That’s the kind of report that forces a broad repricing because it pulls on more than one market theme at the same time. A softer labor market can push yields lower if traders think the Federal Reserve may need a gentler path. It can also hurt risk appetite if traders read the data as a sign of genuine economic weakness. (bls.gov)

Crypto tends to feel that debate more violently because leverage turns macro questions like these into positioning events.

If traders are already crowded into shorts and the macro release eases financial conditions, even briefly, price can snap higher because shorts have to cover.

If the release deepens the risk-off mood, the same crowded book can keep pressing lower because shorts stay comfortable and longs start to give up.

Funding is the pressure gauge, open interest is the fuel, and liquidations are the moment that pressure starts breaking through the system.

Liquidations are the scoreboard

Liquidations tell you whether the move is orderly or forced.

Short liquidations usually confirm a squeeze, and long liquidations usually confirm a flush lower. When both sides get liquidated within a short period, the market is telling you that volatility has taken over, and neither side had much room to hold.

This is why liquidation data works best as a confirmation layer. Funding sets the conditions, but liquidations tell you whether those conditions are actually being forced into price.

Open interest matters here, too. Price can fall, and funding can turn negative without saying much if participation is shrinking at the same time.

That can mean traders are simply stepping back. But when open interest rises alongside negative funding, it means new positions are being added into a bearish or defensive regime.

Tracking open interest in BTC terms removes some of the distortion created by price moves, so rising BTC-denominated open interest during a selloff gives a cleaner read on participation.

Seen this way, the past week was not really about whether Bitcoin was strong or weak, but about where the stress was building.

The derivatives market was already showing a heavy short or hedge regime before the labor data hit.

The jobs report then gave global markets a real macro input to process.

Once those two things met, crypto did what it usually does: it expressed the same macro uncertainty everyone else was dealing with in larger candles, faster reversals, and more violent position clearing.

Funding doesn’t predict price, it just tells you where leverage is leaning. Open interest doesn’t tell you who is right, just how much positioning is still on the field. Liquidations don’t explain the whole move, just when the move stopped being optional.

That’s why derivatives ended up being the best macro explainer of the week. Before the narrative settled, the book had already mapped the risk. Traders were leaning short, leverage was still in the system, and the jobs report gave the market something real to react to.

Everything that came after was price discovering how crowded the room had become.

The post Bitcoin funding rates just flashed one of the bleakest signals in months before one macro number changed everything appeared first on CryptoSlate.